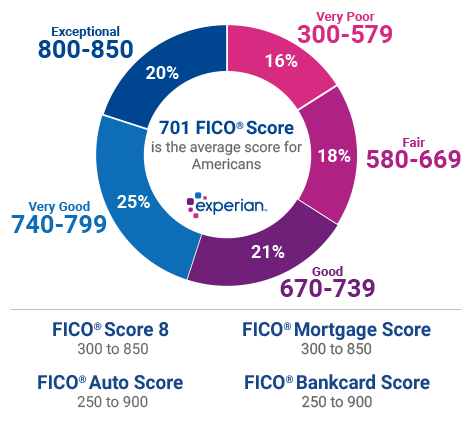

How to Improve Your Credit Score Before Applying for a Mortgage If you’re thinking about…

Inflation Is Leading To Higher Rates

The Federal Reserve has wished for more consumer-price inflation in the past few years. It looks like their wish is finally being granted by the powers able to grant such wishes.

The Labor Department reports that its Consumer Price Index (CPI) rose 0.5% in January. The percent increase was higher than most market-watchers’ estimates. The consensus estimate called for only a 0.3% monthly increase.

Stock prices initially fell on the hot CPI report, but they soon recover. Bond prices also fell, but unlike stock prices, they stayed down. The yield on the 10-year U.S. Treasury note rose above 2.9%. It remains above 2.9% as we write. The yield hasn’t been this high since January 2014.

As the yield on the 10-year U.S. Treasury note goes, so go mortgage rates. Quotes on a prime conventional 30-year fixed-rate loan hit a four-year high this past week. Mortgage News Daily’s latest survey shows that 4.625% has become the predominant quote across the land.

The ascent has certainly been palpable. We entered 2018 with quotes on a prime 30-year loan vibrating in the 4% range. Quotes are up roughly 50 basis points in the past weeks.

Inflation is to blame, though interestingly enough, the CPI isn’t all that heated if we consider the year-over-year change. The CPI shows consumer-price inflation up a tepid 2.1% over the past 12 months.

But of course, the future is what really matters. Maybe bond investors are thinking the latest monthly CPI reading to indicate the year-over-year rate will rise. Or perhaps bond investors take their cue from other data sources.

Another inflation measure, the Fed’s Underlying Inflation Gauge (UIG), shows 12-month inflation growth at 3% in December. That’s the highest rate recorded in nearly 11 years. The last time the UIG measure was this high was September 2006.

Consumer-price inflation remains within the realm of Fed reasoning, according to the CPI. The UIG tells a different story. Perhaps bond investors at least consider the UIG when deciding on portfolio allocations.

The bottom line is that inflation rules the roost these days. Past increases in the federal funds rate (the rate the Fed manipulates) have had little lasting influence on longer-term credits, such as mortgages. Inflation expectations are another story. More market participants anticipate rising inflation, which is evinced in rising yields on long-term credits.

Many borrowers long for mortgage rates that existed only a couple months ago. People naturally anchor their expectations to the recent past. For this reason, a borrower might be tempted to float in hopes better rates will materialize. The journey can be perilous.

The mortgage-rate waters are as treacherous as they’ve been in years. It would be worthwhile to wait for a few days of calm (flat or easing rates) before venturing a float.

The Key Variable for Sustaining the Housing Market

Raising mortgage rates have led to lower mortgage activity. Refinance activity understandably trends lower. Purchase activity has also trended lower in recent weeks. Lower purchase activity has dropped the year-over-year gain to 4%.

Market watchers are concerned rising mortgages will derail the housing market. A Mensa IQ is hardly needed to understand that rising financing costs lower affordability without a compensating drop in home prices.

Of course, affordability can be sustained in other ways, such as through rising wages or additional compensation. The good news is that recent tax reform, which lowered the corporate income tax rate to 21% from 35%, has motivated more companies to either increase wages or offer additional bonuses.

Major companies like Wal-Mart, Comcast, Charter Communications, Apple, Cisco Systems, Delta Airlines, AT&T, Boeing, Home Depot, CVS Health, and others are funneling more money to their employees through higher wages and bonuses. They can funnel more to their employees because lower corporate-income-tax rates means they funnel less to Washington.

Many of these same companies are also funneling more money to their shareholders through increased dividends. It’s fair to assume most working Americans own a dividend-paying stock either directly or indirectly, such as through a mutual fund in a company-sponsored retirement account.

Yes, mortgage rates are higher, but so is borrower income. Therefore, we remain upbeat. We hold our upbeat sentiment with important company.

Home builders remain upbeat as well. The home builder sentiment index posted positively for February. Home builders are particularly upbeat about first-time buyers entering the market. First-time buyers are leading beneficiaries of higher wages and tax-driven bonuses.

*This article does not represent legal interpretation or advice. This is not a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet LTV requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines, and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over life of loan. Reduction in payments may reflect longer loan term. Terms of the loan may be subject to payment of points and fees by the applicant. NMLS: LO# 305371 MB# 761615

Related Posts