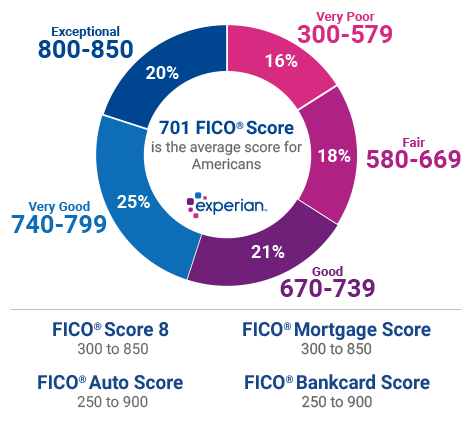

How to Improve Your Credit Score Before Applying for a Mortgage If you’re thinking about…

Tax Law Not Likely To Effect Home Prices

New Tax Law Concerns?

Freddie Mac took a look at some possible effects of the new, Trump-era “Tax Cuts and Jobs Act of 2017” in an early edition of its ‘Outlook’ economic forecast. This month, it takes it’s analysis granular – right down to two families, “the Smiths and the Johnsons”, with both being on the search to purchase a house. The Smiths are an example of a median income family living in Mississippi, while the Johnsons are the example of high income earners living in New Jersey. Each family has one child and both plan to spend four times their income on a home.

Meet the Smiths and Johnsons

The median income Smith’s would actually see little impact from homeownership under the new tax law. Their taxable income would decrease from $17,150 in 2017 to $16,000 in 2018 as the larger standard deduction makes up for the elimination of, or caps on many deductions that might earlier have been itemized. The Johnson’s on the other hand, see their taxable income rise from $198,908 to $250,904. The Smiths enjoy a $115 reduction in their income taxes while the Johnson’s pay $4,300 more. Freddie Mac quotes a study by Zillow that found only around 14% of homes in the U.S. are “worthy enough” for a new homebuyer to benefit from itemizing deductions; down from 44% under the previous tax rules.

The Take-away

Something to consider when worrying about property taxes in Washington state. Seems like the upward swing on property taxes just wont stop. It can be daunting, but hopefully, this will easy your mind slightly, when looking at the numbers on purchasing a new home for your own family. If you still have questions about the new tax implications on your potential new home purchase, talk to Steve Gilbert at Seattle Mortgage directly. He’s always interested in talking to folks to get them on the path to home ownership. You can contact him through the website, email him directly at Steve@SeattleLoanBrokers.com, or call him directly at 206-687-3852.

*This article does not represent legal interpretation or advice. This is not a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet LTV requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines, and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over life of loan. Reduction in payments may reflect longer loan term. Terms of the loan may be subject to payment of points and fees by the applicant. NMLS: LO# 305371 MB# 761615

Related Posts