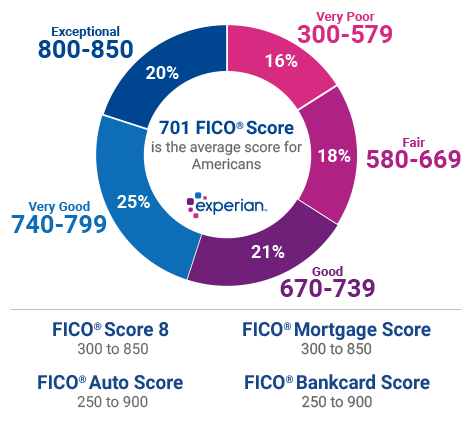

How to Improve Your Credit Score Before Applying for a Mortgage If you’re thinking about…

Is Flipping Hurting The Market?

Flip On Flipping

The data analysis company CoreLogic says “flipping” is back. This fairly well-known term refers to the act of buying, renovating/ repairing a house, then reselling it, all within a fairly short timeframe and usually at a much higher price. Investors who specialize in flipping are always out there, but when prices are on the rise, or appear to be about to go up, a lot more people join in the game.

Bin He, in a post on CoreLogic’s Insights own blog, looked at the current trends of flipping, and using as the criteria a house that is bought and then sold within 12 months. He found that 6.2% of home sales in the first quarter appeared to be flips. This is close the last post-crash high during the first quarter of 2013.

But he also points out it was a different world back then. Prices were just beginning to come back from their 2012 low points, the supply of homes was outpacing demand, and distressed sales had a 30% market share. That share had dwindled to 4.4% at the end of 2017, (and the National Association of Realtors reported on Thursday that only 3.5% of existing home sales in April fit the distressed category.) Inventories are noticeably tight right now, with many home selling after highly competitive bids. Prices? Well everyone knows what has happened there in the last five years.

CoreLogic puts the acquisition cost for a typical flipping candidate at about $170,000 in 2006. That cost bottomed out under $100,000 in the 2011-2012 period. Today it is back to $160,000. He says the high acquisition cost and tight inventories along with rising flipping activity can only mean investors are speculating, betting on continuous home price growth.

Meanwhile, the housing market in King County isn’t really getting better. Seattle’s popularity is on the rise, its getting tougher and tougher to get the house you want at a competitive price. Eventually, it will all balance out. But as to when…that will be left up to time.

*This article does not represent legal interpretation or advice. This is not a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet LTV requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines, and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over life of loan. Reduction in payments may reflect longer loan term. Terms of the loan may be subject to payment of points and fees by the applicant. Seattle Mortgage Brokers, LLC NMLS: LO# 305371 MB# 761615

Related Posts